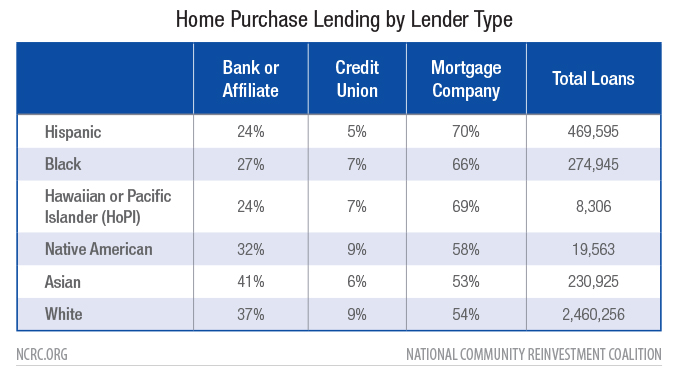

All data used in this report is derived from the 2019 HMDA dataset. NCRC downloads this data from the CFPB and combines it with FFIEC census data, HMDA reporter panel data and OMB CBSA definitions for analysis. Race and ethnicity were identified using NCRC methodology. Unless otherwise noted, the loans used in this report include 2019 applications on owner occupied, 1-4 unit, site built homes. Some outliers have been removed when calculating loan costs, impacting ~1% of the dataset.

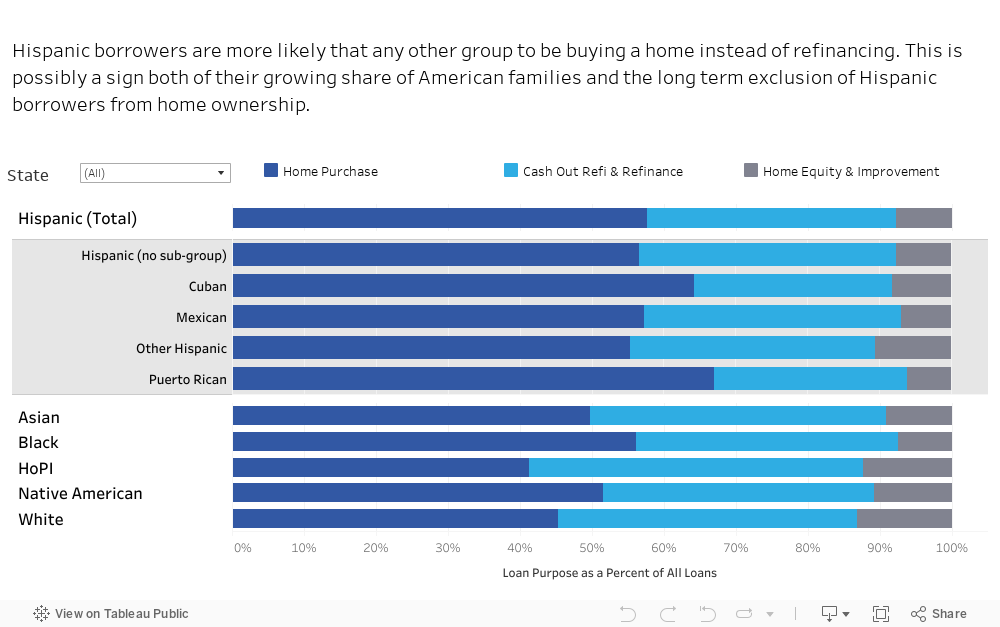

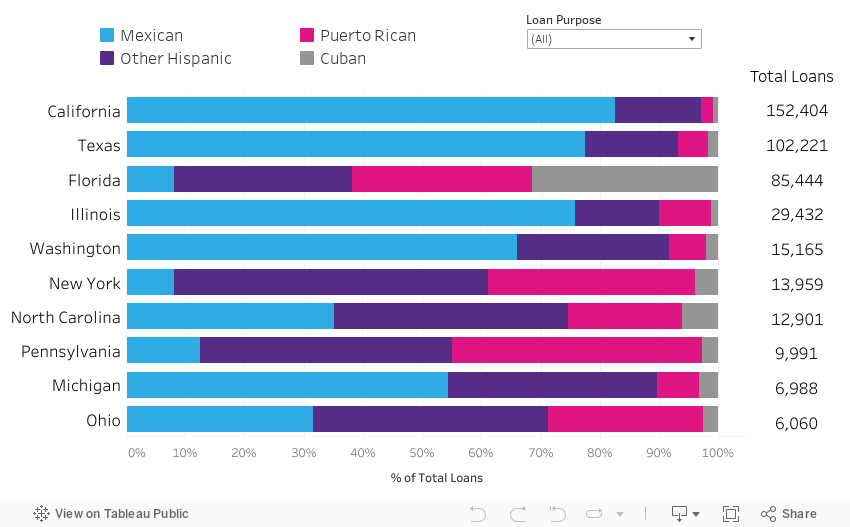

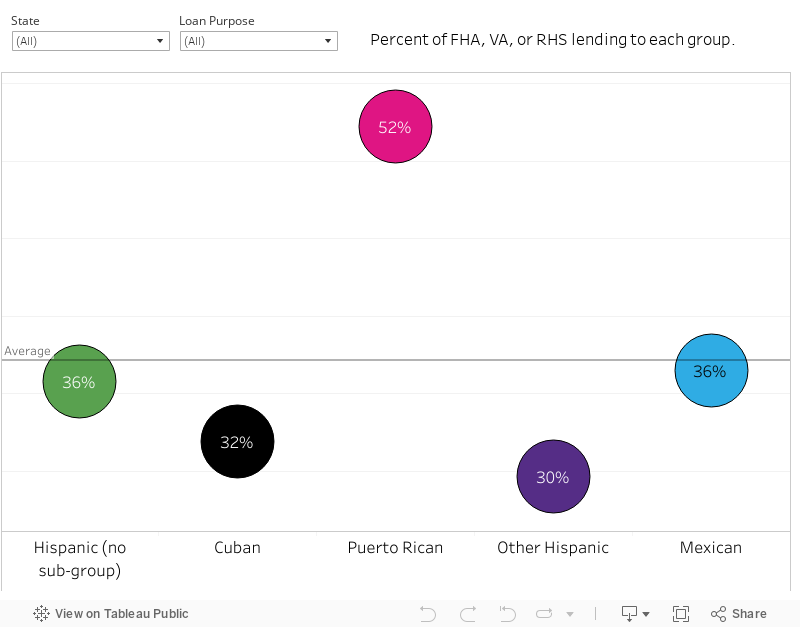

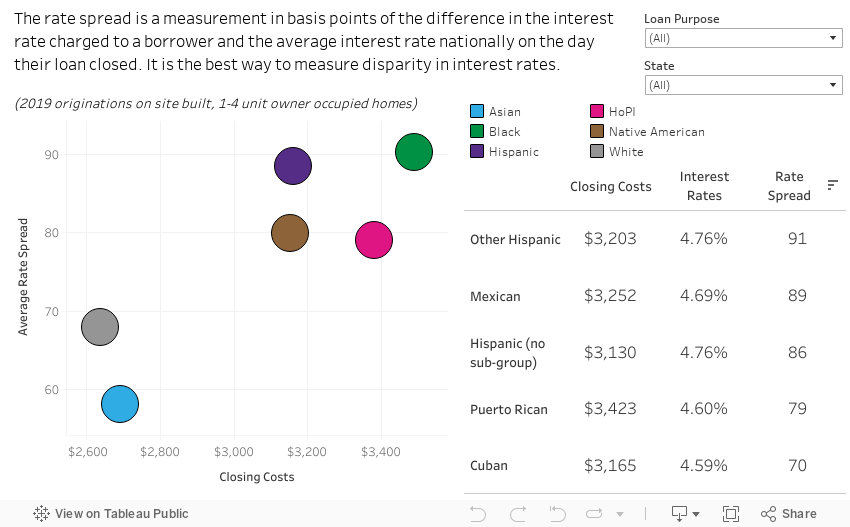

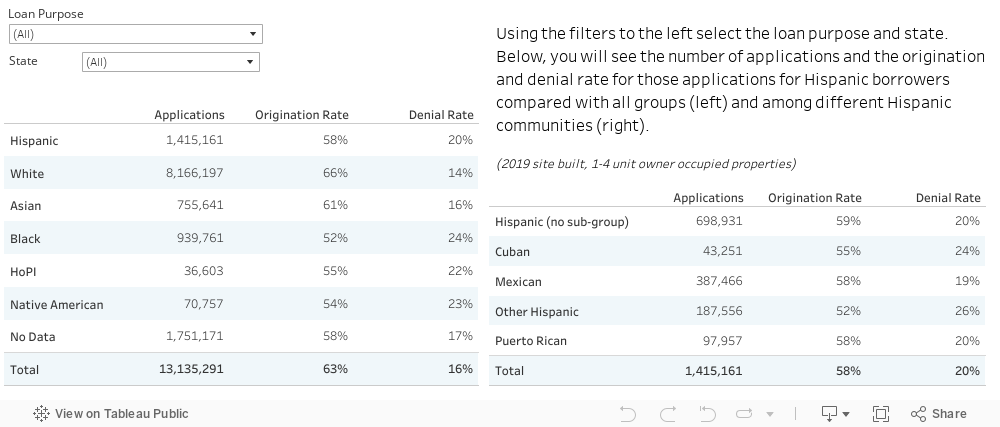

About half of Hispanic applicants in 2019 identified at least one subgroup. We have grouped those that did not indicate a subgroup as “Hispanic (no sub-group).” Definitions of the other groups can be found in the CFPB HMDA documentation.

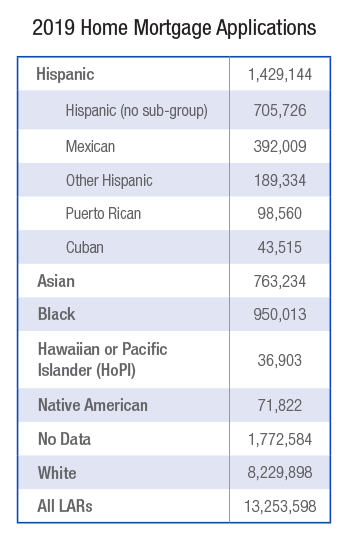

In 2019, there were a total of 17.5 million Loan Application Registers (LARs) reported by mortgage lenders under the Home Mortgage Disclosure Act (HMDA). It is estimated that this data covers about 88% of all mortgage activity in the country. Over 13.2 million loan applications were reported in 2019 for single family properties resulting in 8.2 million originations. Of those applications, there were 1.4 million where the borrower identified as Hispanic which yielded 817,000 originations. The volume of loan applications from Hispanics was the second largest of any racial group after non-Hispanic White applicants.

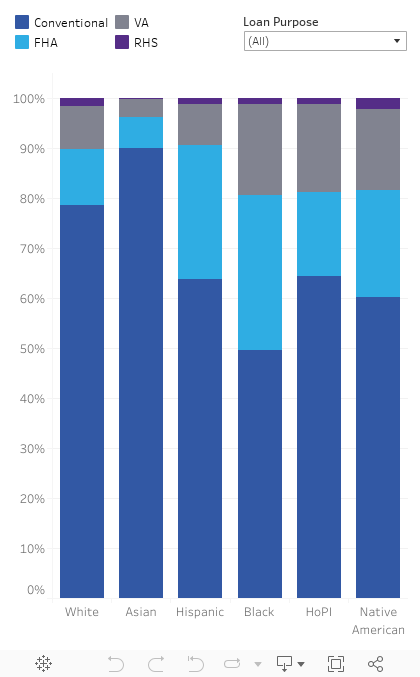

The secondary mortgage market also plays an important role in facilitating borrowers’ access to a mortgage. Mortgage entities like Fannie Mae and Freddie Mac (together, the GSEs) purchase mortgages made by lenders, and design mortgage programs with features like lower down payment requirements that make home lending more affordable to communities that have historically been priced out of homeownership opportunities. Through these affordable loan programs, lenders are provided liquidity and guidance on eligible loan terms and conditions to encourage them to serve borrowers from lower wealth or low-income communities.

These programs also have an impact on Latinos’ access to conventional products, which may also affect mortgage payments over the life of the loan, including better interest rates and opportunities to cancel mortgage insurance fees. In 2019, one-quarter of loans originated to Hispanic borrowers were purchased by the GSEs, another 17% included FHA loans that were securitized by Ginnie Mae, and 35% in the category of Other, which included loans purchased by investors or other lenders.

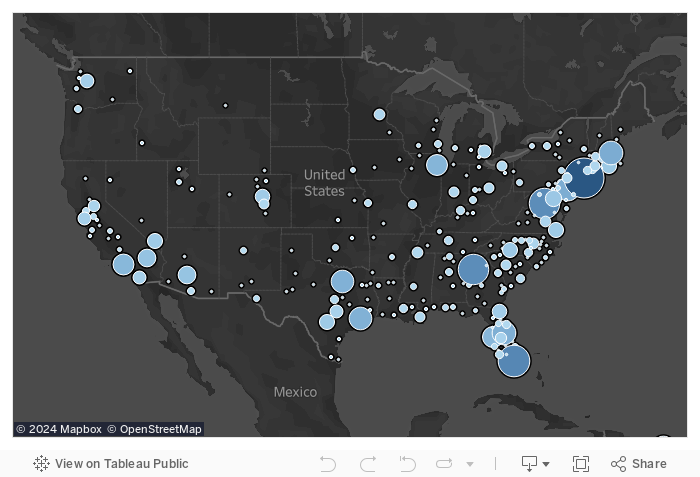

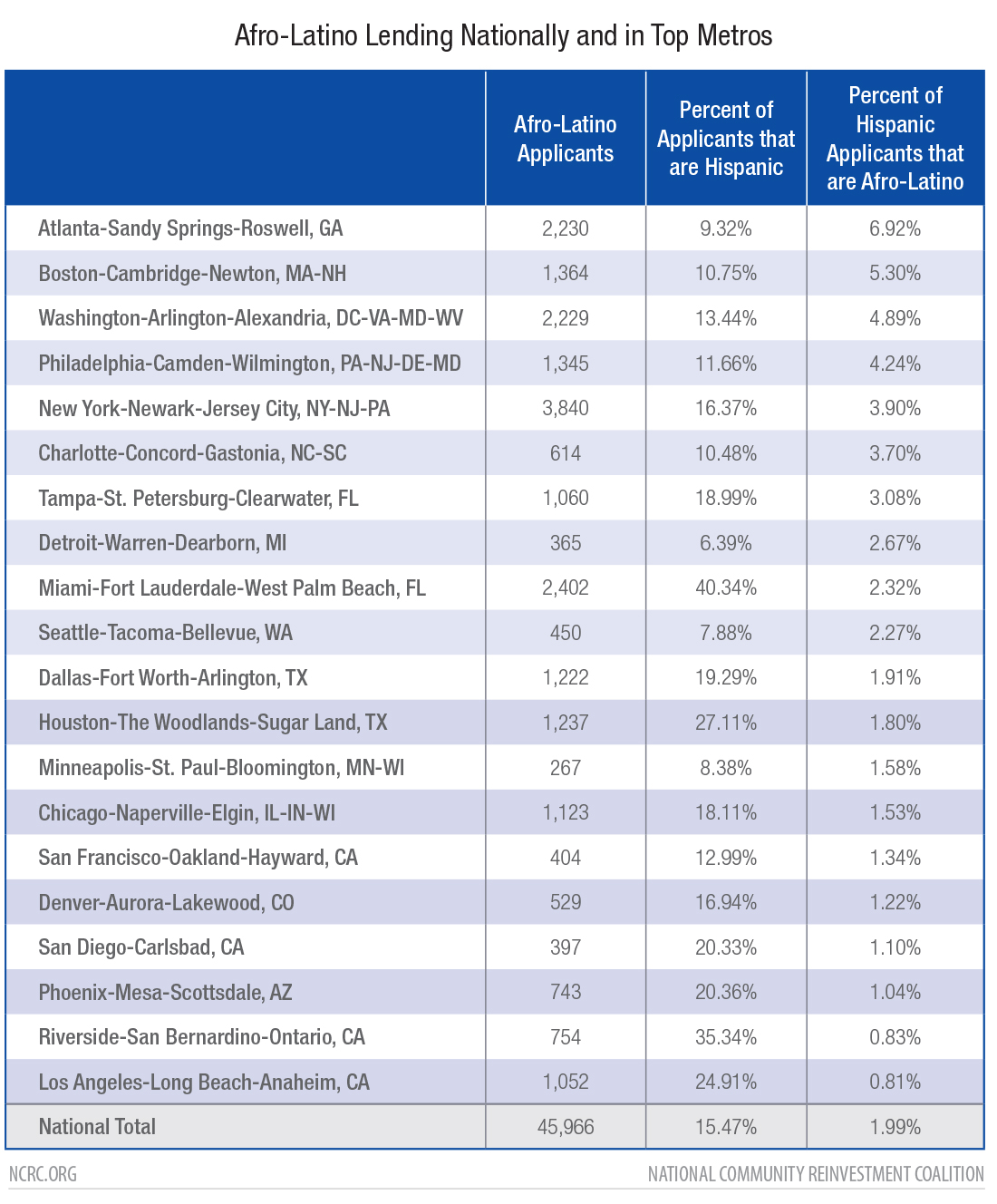

Afro-Latino Lending Map, 2019 application where the applicant or co-applicant reports both a Hispanic ethnicity and Black race.

Among the areas studied, the most applications were received in the metro areas of New York City, Atlanta, Washington, D.C., and Miami. In the New York-Newark-Jersey City metro area, over 3,000 Afro-Latinos applied for a mortgage. While Hispanic applicants consisted of less than 1% of mortgage applicants in the area, Afro-Latinos made up about 4% of all Hispanic applicants overall in the area. The same was true of Afro-Latino applicants in the Atlanta-Sandy Springs-Roswell metro area, where Hispanic applicants were less than 1% of applicants. In 2019, over 2,000 Afro-Latinos applied for a mortgage, representing about 7% of all Hispanic applicants in the area.

Even in metro areas including Boston, Orlando and Dallas, where about 1,000 Afro-Latinos applied for a mortgage, these applicants represented a substantial share of Hispanic applicants.

Notably, the metro areas where Afro-Latinos are applying for a mortgage are among the most expensive in the nation. More research is needed to understand the experiences of Afro-Latinos, who are likely facing barriers of high housing prices and borrowing costs when encountering the mortgage market.

These trends demonstrate the growing importance of Afro-Latinos in these mortgage markets, as well as a signal of growing interest in homeownership among these communities.