NCRC Calls For Federal Investigation Into Lenders’ Refusal to Make Loans to Working Class Families

Files 22 Complaints With HUD Over Lenders’ Unfair & Discriminatory Policies

WASHINGTON, DC — The National Community Reinvestment Coalition (NCRC) today called on federal agencies and banking regulators to investigate the nation’s largest Federal Housing Administration (FHA) approved lenders for possible violations of federal housing rules by refusing to offer loans to qualified Americans to the FHA policy of a minimum credit score of 580 and above with a 3.5% downpayment.

A recent NCRC investigation found that the majority of top FHA lenders failed to offer applications for federal-guaranteed loans to potentially qualified borrowers with credit scores below 620 or 640, even though FHA guarantees loans with credit scores to 580. These lenders have policies that establish “credit overlays” above the FHA policy, with minimum credit score requirements as high as 640. One-third of all Americans have credit scores under 620.

“Critical to our nation’s economic progress is the ability of homeowners to get quality refinancing, and for homebuyers to reclaim vacant houses by accessing quality mortgage credit, ” said John Taylor, president & CEO of the National Community Reinvestment Coalition.

“The decision by some banks to not follow the FHA’s policy is cutting qualified borrowers off from accessing credit, and in doing so, causing harm to their ability to prosper, build wealth and for our economy to grow. And this decision is arbitrary, because the loans are 100% guaranteed, whether the borrower’s credit score is 580 or 780. That means the loans with lower credit scores don’t pose additional risk to the company, so there’s no legitimate business defense for this across-the-board practice. A lender is only at risk if they fraudulently or improperly originated the loan, against FHA’s underwriting criteria. As is the case across the secondary market, in that situation, the lender can be forced to buy back the bad loan,” said Taylor.

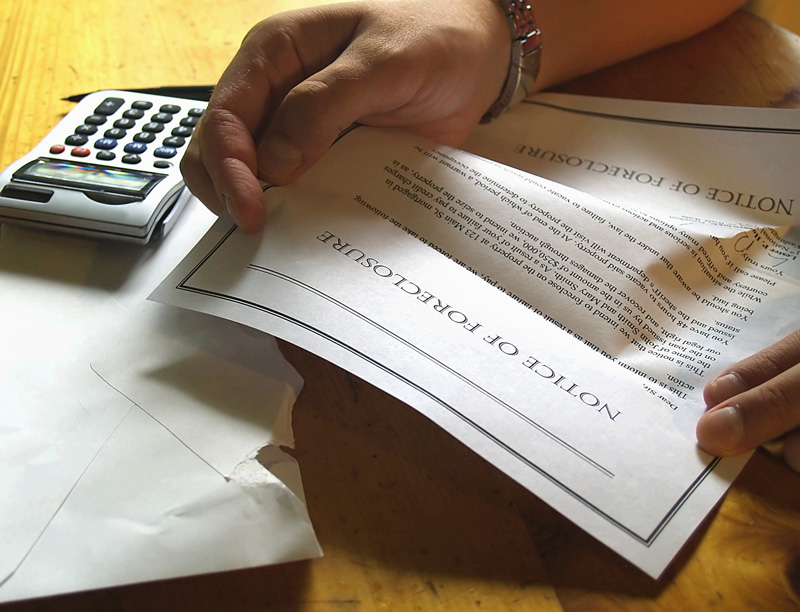

Crisis Inquiry Commission report

Crisis Inquiry Commission report groups in a call for a temporary national moratorium on foreclosures, until an investigation can be completed to determine the extent to which consumers’ rights have been violated by servicers and lenders. NCRC also called on Congress and the Administration to pursue non-voluntary measures to resolve the foreclosure crisis.

groups in a call for a temporary national moratorium on foreclosures, until an investigation can be completed to determine the extent to which consumers’ rights have been violated by servicers and lenders. NCRC also called on Congress and the Administration to pursue non-voluntary measures to resolve the foreclosure crisis.